Consensus and Dissent in Investment Committees

Consensus and Dissent in Investment Committees

How VC Firms Make Great Investment Decisions

🔈 As an experiment, I created a podcast version of this post using Google’s Notebooklm service. It’s a fun listen! Check it out in the audio player below or read on for the full article.

One of the most engaging aspects of working at a venture capital firm are the lively debates of whether to invest in a startup. The best discussions are intellectually rigorous and push investment teams to uncover the true potential and risks of an investment opportunity.

These inner-firm dialogues offer valuable insights into how a partnership works. Although every team will have some version of an investment committee (IC) – a formalised group of partners or senior investors who facilitate and approve investment decisions – each firm’s approach varies depending on culture and whether it’s an early or late-stage investor, to name but a few variables.

What’s the best approach for ICs to maximise decision-making quality and financial returns? There are no hard rules. However, my research on how exceptional firms operate revealed two broad contexts, each requiring a different mindset and approach.

The Voting Duality

At the atomic level, there are two classes of investment decisions at an IC: the consensus approach and the champion rule. Both can be successful, and it isn’t unusual to find firms with different philosophies within the same business. For this reason, it’s helpful to think of the consensus approach and champion rule as two ends of a spectrum, each with its advantages, risks, and quirks. Here’s a brief overview of the two systems.

Consensus Approach: This method requires a simple majority or unanimous agreement in a partnership for an investment to move forward. It benefits from collective wisdom but risks averaging decisions out in favour of conventional rather than bold bets.

Champion Rule: This approach encourages dissent and individual conviction. If one or a few partners have firm convictions about an investment, it gets approved even if most of the IC isn’t convinced. This decision-making style is conducive to investing in bold ideas, but too much individual enthusiasm can temper critical evaluation.

Few VC firms are religious about any one method. Most teams operate on a spectrum ranging from consensus to conviction, adapting their approach depending on context. Still, there are some broad principles about what works best and when. Here’s a brief look at each philosophy and where it excels.

Pre-seed & Seed: The Champion Rule Dominates

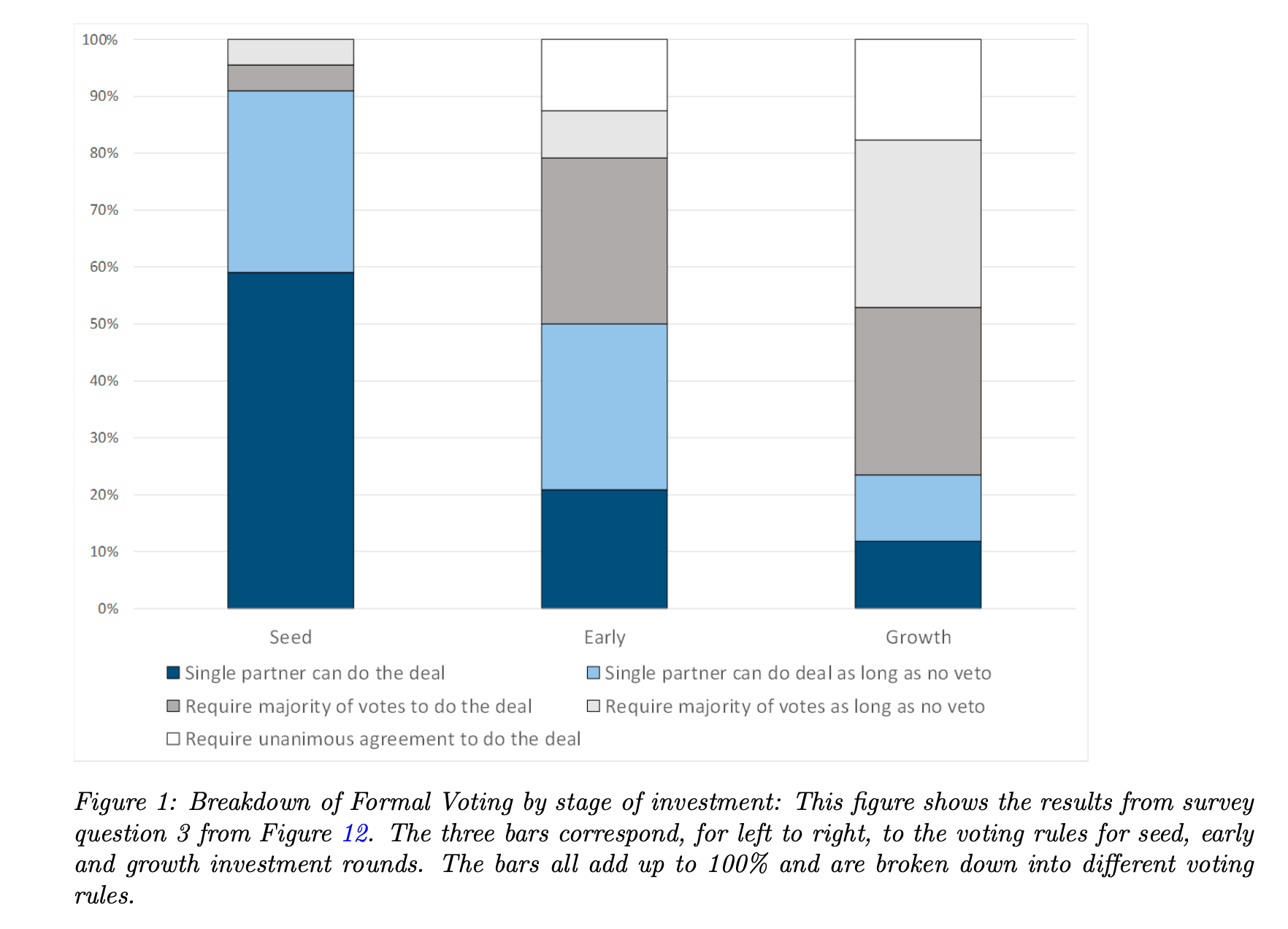

A survey of US VC firms conducted by researchers from Imperial College London, MIT, Harvard and the University of Michigan found that 90% of seed-stage investors use the champion model or some variation of it. This fraction drops to 50% for early-stage investors (Series A to B) and roughly 20% for growth-stage investors.

VCs generally favour the champion rule at the earliest stages of investing but shift to consensus at later stages. Why? It’s all about “catching outliers,” as explained in this research paper by Malenko, Nanda, Rhodes-Kropf, and Sundaresan. Their simulations show that the champion rule is 3.7 times more likely to catch a ‘unicorn’—a startup generating a 10x return or higher—compared to unanimous decisions and 2.7 times more effective than the majority vote approach.

The reason behind this lies in the highly skewed nature of returns in early-stage investing, where the distribution of profits follows a fat-tailed, subexponential pattern. In such distributions, a small number of outlier companies drive the majority of returns. Therefore, early-stage investors need decision-making processes that can approve high-conviction opportunities, particularly when the partner championing the deal has specialised knowledge or unique insights about a company’s potential.

Encouraging individual conviction enables a VC firm to back more of these outlier companies, even if they exhibit flaws that a consensus vote would reject. The key here is to try and minimise “false negatives”. They are more costly than “false positives”. Put another way, it’s far worse to reject a potential WhatsApp (sold for $19bn) than to back a venture like Vine, which was eventually eclipsed by newer platforms like TikTok, or General Magic, which failed to gain market traction despite pioneering ideas later seen in the iPhone. Champion rules allow funds to cast a broader and less conservative net that can capture more of these unique opportunities.

Another noteworthy phenomenon is that early-stage investing is prone to the “catastrophe principle”. (Despite the negative-sounding name, this term is neutral in mathematics.) It provides some explanation as to why the champion rule is effective. In catastrophe theory, a few underlying factors can lead to sudden, disproportionate outcomes—a concept originally used to model behaviour in natural systems. In the context of early-stage investing, this principle reflects how the success of a startup is often driven by one or a handful of exceptional characteristics (e.g. market timing or generational talent), while other traits may be average or even flawed. The champion rule allows an investor with conviction to proceed based on these “superstar” traits, which a committee is more likely to dismiss with a consensus-based approach.

The excerpt below, from a 2014 Harvard Business School case study on Andreessen Horowitz, summarises the rationale of a champion philosophy in practice:

“GP Jeff Jordan described the firm’s investment criteria: “We look for strength rather than lack of weakness. It’s easy to point out what’s wrong with a deal, particularly when you say ‘no’ 98% of the time. We want a passionate advocate—at least one general partner who is just pounding the table to do the deal.”

Andreessen concurred: “Google, Facebook, eBay, and Oracle all had massive flaws as early-stage ventures, but they also had overpowering strengths. Some VCs have all their partners score a deal’s potential. We’ve learned that those aggregate scores don’t correlate strongly with ultimate returns. With that approach, you get the mush in the middle, with no great strengths but no big flaws.” Ultimately, any a16z GP could make a “go” decision if he or she felt strongly; the cofounders did not serve as tie-breakers, nor did they reserve veto power. a16z’s review process was different from that employed by many other VC firms, where partners invested only after majority votes and after their “silverback” failed to exercise his or her veto.”

Other investors agree. For example, Mike Maples at Floodgate is careful to highlight the issues with some voting systems, such as politics (‘if you vote for my deal, I’ll vote for yours’), groupthink, and the risk of consensus killing the “magic of what causes somebody to have insight of a great startup before the world believes,” as he put it to Harry Stebbings on the 20VC podcast.

According to Mike, some of their best investments seemed crazy at the time but eventually paid off. For instance, it was unclear whether Twitter – a product focussed on 140 characters – was even a product. It had no revenue model or clear roadmap. Twitch was initially a guy with a camera on his head. Cruise Automation – a promise of driverless cars – seemed like science fiction in 2014. But at Floodgate, they proceed with an investment if one partner has enough conviction to “pound the table” about it. This limits the conservatism of consensus and opens the door to more unconventional and potentially outlier investments.

The championship model has some clear weaknesses, though. Betting on one person’s conviction without guardrails and sufficient due diligence can be disastrous, particularly if their conviction is misplaced or has an ulterior motive. There’s also the issue of accountability and blame games, but smart teams know how to mitigate these issues.

For example, the London-based seed fund LocalGlobe is conviction-driven, but deal champions seek input from an IC and the broader investment team. This helps investors identify critical areas for due diligence and aspects of an opportunity that one person alone might miss.

Once a decision is made, the entire firm stands behind it. “There’s no ‘I told you so’ if something goes wrong,” says LocalGlobe investor Emma Phillips in an interview with Sifted.

Series B and Growth Stages: Consensus Works

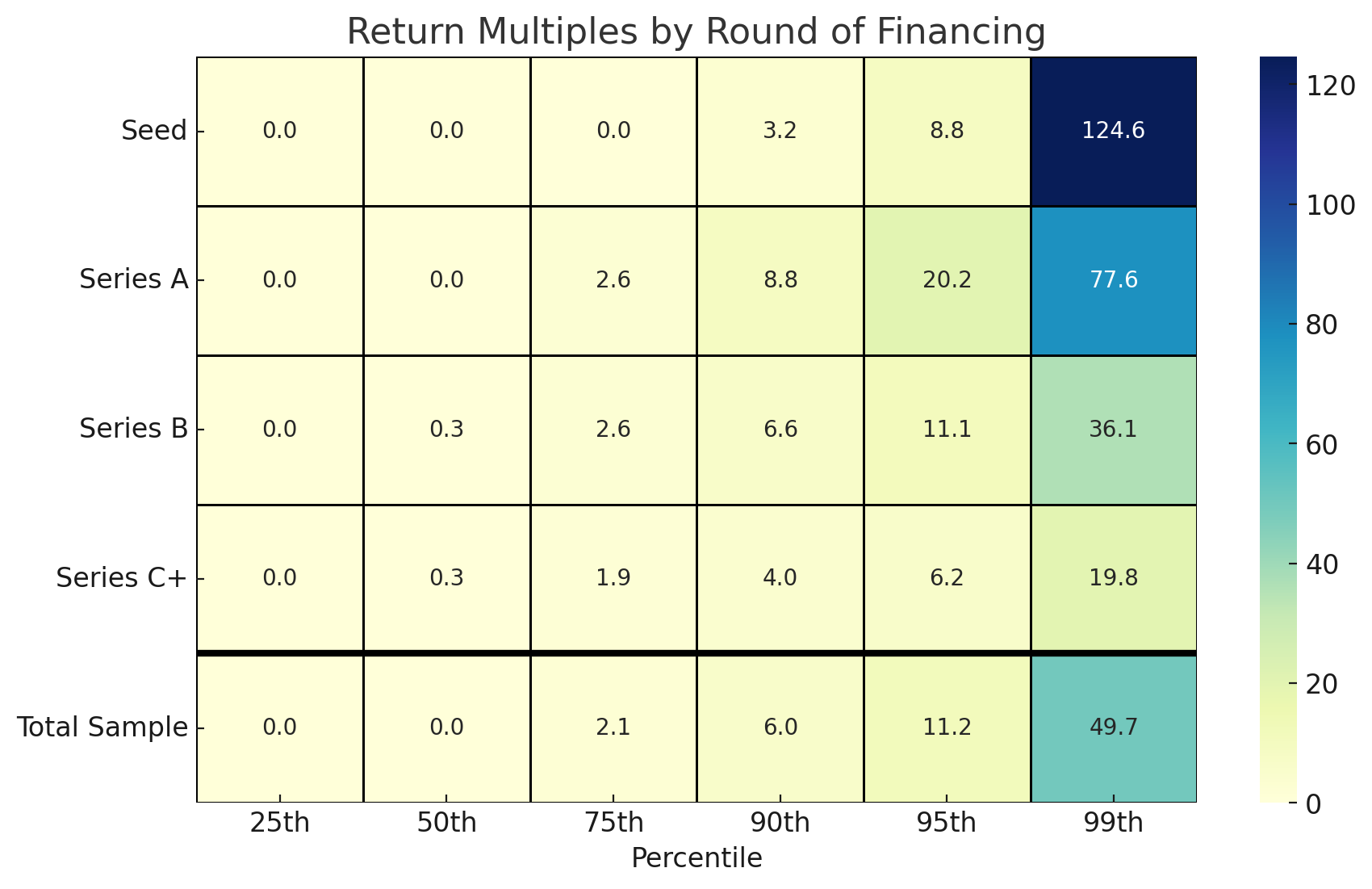

As startups progress to later stages, returns are less skewed (see the chart below). In this realm, consensus at investment committees is more effective. This is because the focus shifts from catching outliers to making balanced decisions. There’s less uncertainty, more data to interrogate, and several qualities everyone can agree on, such as revenue growth, customer retention, market adoption.

The consensus approach and majority voting also have strong theoretical and empirical underpinnings that suit certain environments. For example, in the research paper I cited earlier, the authors highlight Condorcet’s Jury Theorem. It posits that if each person in a decision-making group is well-informed and has a better-than-random chance of making the right call, then the probability that a collective will make an effective decision increases as the group grows in size. However, this only works well if each decision-maker is independent and isn’t biased.

Returning to the world of VC, you’ll find many firms that adopt various voting processes to aggregate information and distil it into a concrete decision. For example, Index Ventures employs a uniquely structured voting mechanism. According to Dany Rimer, “Every investor has a vote, and we have a voting system that goes from 1 to 4 and from 7 to 10, so you can’t do a 5 or a 6, and you need a certain threshold of positive votes north of 6 to get an investment past through the partnership.” While this system utilises consensus, it also ensures that the partner presenting the deal shows strong conviction: “If someone comes in with a 7, it’s going to be difficult unless it’s unanimous. Our best decisions have always been unanimous.”

At Sequoia Capital, they thrive on radical candour and open disagreement. There’s the added nuance of each partner having veto power as well. That said, they encourage independent judgement by using a blind voting system. Sequoia’s managing partner, Roelof Botha, also drives diversity of thought by occasionally asking his team to reargue investments if he feels that a partner is being too positive too quickly. This culture ensures that decisions reflect a true consensus built on rigorous debate rather than superficial agreement.

What’s the Best Approach?

There’s no simple answer here. Although the theory (and some empirical findings) suggest that the champion rule works best at the earliest stages of investing and that consensus is more effective in growth-stage investing, you’ll find numerous exceptions and counter-examples in the VC industry.

For instance, Union Square Ventures are fantastic early-stage investors, but their decision-making involves consensus-driven discussions. In a 20VC interview, partner Andy Weissman mentioned that they do not vote. However, they “have a conversation, and that conversation leads to a point where everyone is comfortable with the parameters of an investment,” says Weissman. This informal, dialogue-focused method emphasises the importance of shared understanding over rigid voting systems or individual agendas. And it probably works well for USV because the partnership is small, nimble, and built on significant trust.

Benchmark takes a similarly flexible approach. As partner Eric Vishria explained on 20VC, “Our process is built on advocacy and voting.” While one partner may support a deal, the team uses a voting system to gather different perspectives. So even if the votes are split—as was the case with eBay and Red Hat—the partnership can still approve an investment. However, like LocalGlobe, all partners engage deeply and contribute to the due diligence process when a deal is approved. This mix of advocacy and voting facilitates consensus while preserving individual conviction.

Finally, the multi-stage firm Founders Fund, which primarily invests in Series A and B, adjusts the level of consensus required depending on cheque size. Brian Singerman notes, “The larger the check the more, shall we say, votes you need.” This structure aligns the level of scrutiny with the size of the commitment. It seeks more consensus for later-stage investments while enabling fast, conviction-driven, decision-making on smaller bets.

Finding What Works in a VC Firm

Most firms iterate to a system that works well for them. There’s no one-size-fits-all. You need to consider the investing stage of a firm (early-stage vs. late-stage), team dynamics (number of investors, culture, skills and experience), and market focus (established vs. emerging industries).

Early-stage firms hunting for the next unicorn may benefit from bold bets enabled by the champion rule and a culture of individual conviction. At the same time, growth-stage investors may do well in aggregating insights from spirated debates and consensus views. No matter the case, successful firms often combine elements of both, blending conviction with group wisdom to navigate the inherent uncertainties of startup investing.