Is Venture Capital a Game of Luck or Skill?

No venture career gets minted without luck.

Hi all! If you’re already a subscriber feel free to dive right into this week’s edition. 👇🏾

If you’re new, a warm welcome and thank you for subscribing! This newsletter shares the best VC wisdom and knowledge curated from seasoned investors, researchers, and technologists.

You’re part of 250+ industry insiders who’ve joined along on a journey to mastery & impact.🚀

Early-stage investing is remarkably stochastic. “I’ve made tons of money on things I thought were dead. And I’ve had things I thought were amazing go to zero.” That’s the former VP of Product at Facebook, now turned investor, Sam Lessin. In this podcast interview, Lessin reiterates a fact that all VCs have to grapple with: “There’s a ton of random walk.”

If you consume enough content about venture, you’ll hear multiple versions of this truth. But is venture capital success really a game of luck or skill? Let’s untangle the question with something anecdotal but representative of the nuance involved.

One of Sequoia’s most successful investments is WhatsApp. Facebook paid $22 billion for the business in 2014. Sequoia’s first investment in the company was just $8m in a Series A round. The fund would invest a further $52m before the Facebook acquisition, which returned $3bn to Sequoia.

How did Sequoia source, select, and secure an investment in this incredible business? Hustle and smarts. The co-founder and CEO of Whatsapp, Jan Koum, had no interest in meeting with investors. Sequoia’s Jim Goetz had to court the founder for two months to get him over to Sequoia’s offices. But before that, Goetz had led a brilliant initiative at Sequoia called “early bird”, which tracked app store downloads globally and identified WhatsApp as a promising prospect. This was before data-driven VC was even a thing. Sequoia hustled and worked hard to make this investment.

Yet, a foundation of historical luck is critical for any fund to have the opportunity to invest in a company like WhatsApp. Here’s how Jan Koum of WhatsApp recalls his decision to take money from just this one VC fund:

“I think Sequoia, in general, first of all, has been an amazing partner for us. But I think if you look at the history of Sequoia, you know they’ve supported companies like Cisco and Apple and Google, and Yahoo.

Growing up in Silicon Valley — and I’ve lived here for 22 years — there’s this heritage that Sequoia has and pedigrees that a lot of other venture funds don’t have.

And I remember sitting (after we got a few different term sheets), talking to Brian, and I was like, ‘Brian look, five years ago, if someone had told us we would have a term sheet from Sequoia when we were starting this company, nobody would believe us – we wouldn’t believe this ourselves. And now we have this opportunity, we should just do it and go for it.’

We also got some advice. Geoff Ralston, who was one of our coworkers at Yahoo, I remember me and Brian drove over to Geoff Ralston’s house. It was like 11 pm. It was like a scene from a James Bond movie because nobody knew about us, and we didn’t want to tell anybody that we were raising. We didn’t wanna get any attention. We got to his house at 11 pm when everybody was asleep, and Geoff was kinda looking at various term sheets, and he was like, ‘a Sequoia company is always a Sequoia company,’ and we were like, okay, well, that makes sense.”

In venture, early success begets more success. Preferential attachment — a phenomenon that plays out in venture when the best founders partner with already successful funds — contributes massively to different outcomes. And because Sequoia had a history of backing winners, WhatsApp chose to partner with them.

What were those early successes for Sequoia? The first investment out of its $5m debut fund in the 70s was the iconic video game pioneer Atari. The second investment was Apple. Talk about a flying start!

As a semiconductor industry veteran, Sequoia’s founder, Don Valentine, had undisputable skill and talent. No one wanted to invest in Atari but he was bullish about its prospects, so he rolled up his sleeves and got involved. He added value to the investment when he introduced Atari to Sears, a national chain of department stores. This introduction paved the way for a game-changing distribution deal that accelerated Atari’s trajectory. The video games company eventually sold to Warner for $28m, generating a 4x return for Sequoia.

Was that luck or skill? The selection of the investment and value-added were clearly skill. But what were the circumstances in which the deal was found? You’ll find a long trail of happenstance that provided a foundation for success. From Don Valentine being introduced to Atari by a former colleague at Fairchild Semiconductor, to being in the right place (in Silicon Valley) at the right time (the semiconductor and microprocessor boom years.)

How about Apple? This was Sequoia’s second investment. It yielded a 30x return after the IPO in 1980. How much of this was luck versus skill? Sequoia worked hard to make the investment pay off, but I would argue that finding this deal also had elements of luck and involved being in the right place at the right time.

You see, Steve Jobs was an early employee at Atari before founding Apple. And it was Atari’s CEO Nolan Bushnell who introduced Steve Jobs and the Apple investment to Sequoia’s Don Valentine.

How did Steve Jobs end up at Atari? Serendipity. He found an ad in the San Jose Mercury, buried among dozens of ‘help-wanted’ job postings. The listing read, “Have fun, make money,” and was for a position at Atari. Steve went for it and became a notable employee at the company.

According to Atari’s founder, it was Steve Jobs who found Atari, not vice versa. And not just that, but the hiring engineer Al Alcorn, who first met Steve and gave him a chance, had this to say:

“I was told, ‘We’ve got a hippie kid in the lobby. He says he’s not going to leave until we hire him. Should we call the cops or let him in?’ I said bring him on in! . . . In retrospect, it was weird to hire a dropout from Reed. But I saw something in him. He was very intelligent, enthusiastic, excited about tech.”

Without Atari taking a chance on Steve, he might have never met Don Valentine. But also, without Don Valentine skillfully investing in Atari, he might have never fortuitously met Steve Jobs.

Luck and fate play a role in every aspect of life, and venture returns are especially sensitive to seemingly innocuous events that, in hindsight, play a massive role in outcomes.

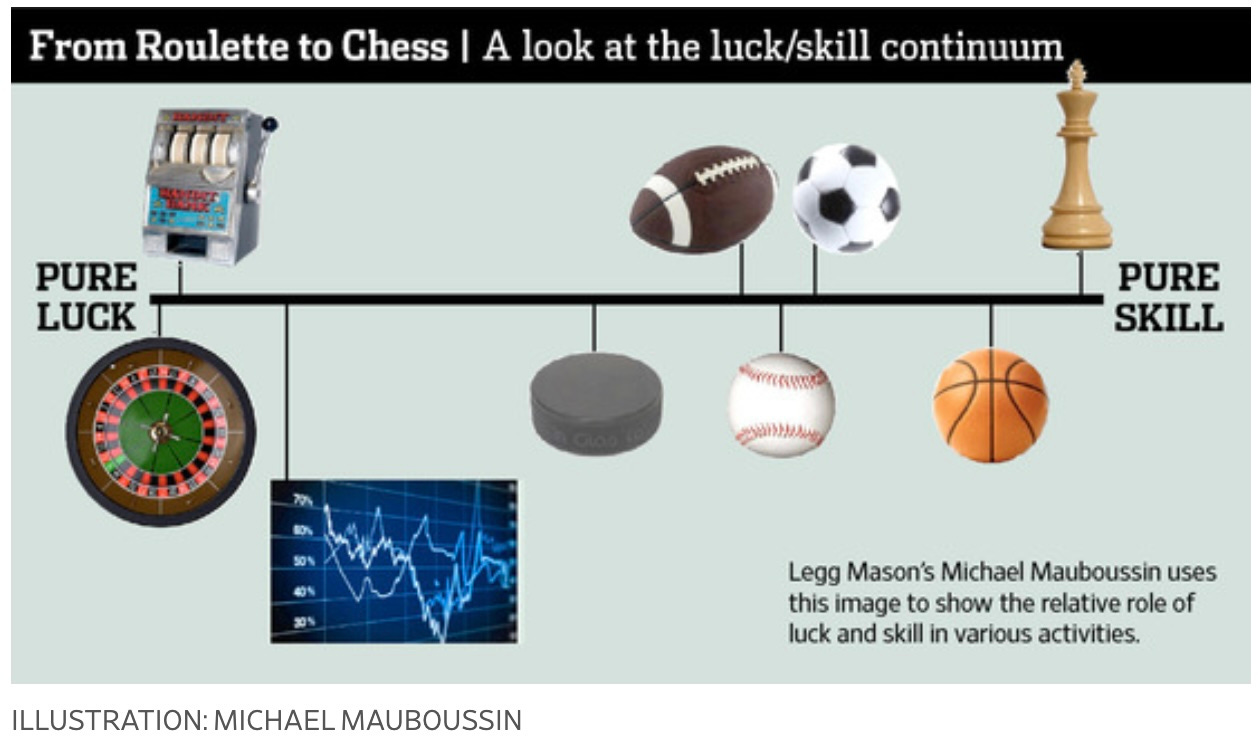

Does that mean that venture is all about luck? Not exactly. In fact, we can use a simple litmus test to determine whether early-stage investing is 100% luck. This is best summed up by the investment practitioner and researcher Michael Mauboussin, who writes:

“...ask whether you can lose on purpose. In games of skill, it’s clear that you can lose intentionally, but when playing roulette or the lottery you can’t lose on purpose.”

You can definitely lose all your money on purpose in venture capital. Put it all in the bottom quartile of entrepreneurial talent and outlandish businesses, and you’ll barely make it past a year or two of an investing career. In contrast, try losing every game of roulette. It’s impossible.

If you can lose money on purpose in venture it means that there’s an element of skill that can boost your chances of generating returns. We’ve seen some examples with Sequoia’s Atari and WhatsApp investments, but we’ve also seen how chance events can be historic.

In upcoming issues of VC Mastery I’ll write more about the skill aspect of venture, but also expect a mix of content on how to drive luck, given its role in the craft.

Venture is a game of perseverance, process, and purpose. You win by playing the long game, capitalizing aggressively on early successes (and luck), but never resting on your laurels once you’ve had a few hits. Just as luck can propel you ahead, reversion to the mean (which amounts to underperformance in venture) is never more than a few investments away.

I’ll close with a practical takeaway from an interview with researchers who’ve looked at how success breeds success in venture capital. The excerpt is shared verbatim from a Yale Insights conversation with Olav Sorenson, co-author of the paper, ‘The persistent effect of initial success: Evidence from venture capital’.

🥡 Practical Takeaway:

Interviewer: If the first win is dumb luck and subsequent successes flow from that one, does that change the approach that VC investors should take?

Sorenson: It does suggest that what a new VC might want to do is really kind of swing for the fences. If you’re trying to take sure bets, or at least relatively low-risk investments, then you might have some success in terms of your overall average return, but you won’t have these kind of really well-publicized, highly visible successes that seem to be what are responsible for establishing the reputations that get other entrepreneurs to want you as an investor. It does suggest an approach where, well, I’m going to try taking some really big bets. If they go well, I could potentially be set up for my next fund. But if not, I probably don’t have a future in the industry.

This is something I will never forget!

"If you can lose money on purpose in venture it means that there’s an element of skill that can boost your chances of generating returns."

Fred Destin wrote a good post about this yesterday.

See here https://www.linkedin.com/posts/freddestin_for-younger-investors-heres-some-hard-shit-activity-7153053020740591617-G7KZ

And my comment reply https://www.linkedin.com/feed/update/urn:li:activity:7153053020740591617?commentUrn=urn%3Ali%3Acomment%3A%28activity%3A7153053020740591617%2C7153291942620012544%29&dashCommentUrn=urn%3Ali%3Afsd_comment%3A%287153291942620012544%2Curn%3Ali%3Aactivity%3A7153053020740591617%29