The Upside of Liquidation Preferences

Most people think liquidation preferences are just about the downside. However, there's an upside thrust to the instrument that's easy to miss.

A lot of VCs believe that liquidation preferences are all about downside protection. But while this is an explicit justification for the instrument, it misses an important point: Liquidation preferences are more about encouraging the upside than they are about getting whatever little money you can out of a low-exit startup scenario. Why’s that the case?

Let’s start with the basics. Most VCs get shares with a liquidation preference when they invest in a startup. (Over 80% of Series-A and later-stage investments in the UK have liquidation preferences compared to just under half of seed deals.) This means that when a company is sold, the VC gets paid ahead of ordinary shareholders. I’ll spare further details here, except that in an IPO situation, the preference falls away, and everyone splits the proceeds according to their shareholding percentage.

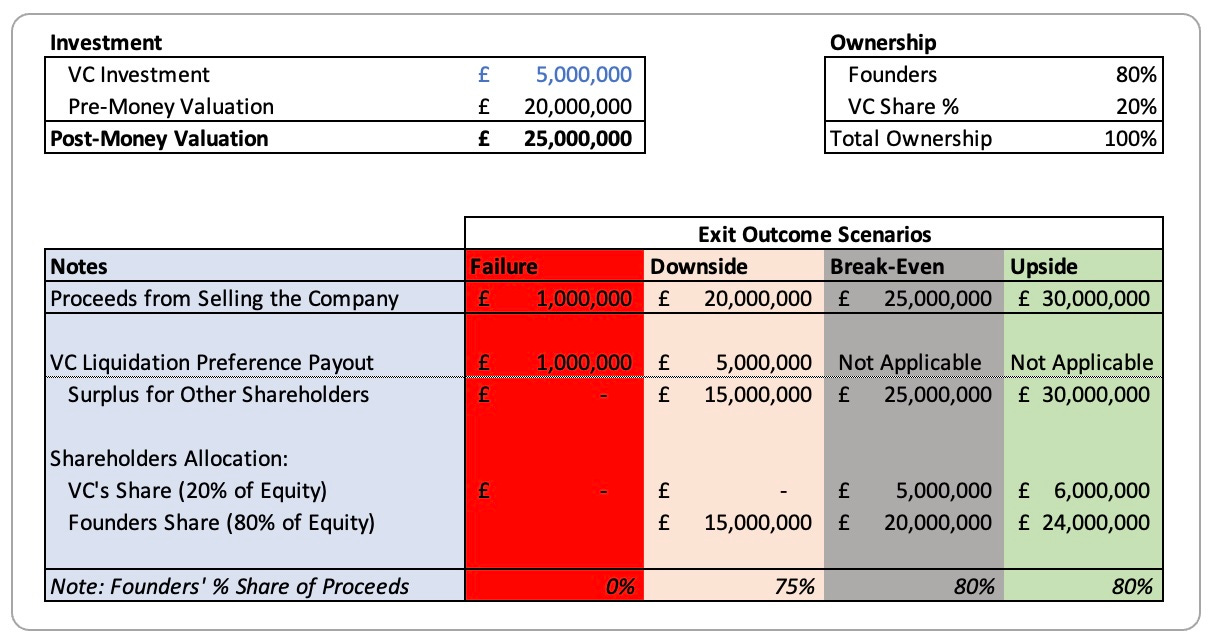

Here’s what a simple exit scenario might look like. Let’s say a VC invests £5m into a startup at a £20m pre-money valuation and with a 1x liquidation preference (You can learn more about the different types of liquidation preferences here). Under different exit outcomes, the payouts would look like this:

Notice that the VC is protected in the low-exit scenarios. The investor is paid first when the company sells for anything less than the post-money valuation (£20m pre-money + £5m investment = £25m post-money). In that situation, regular shareholders get proportionally less than they would have been entitled to had the VC acquired ordinary shares. That’s the downside protection most VCs talk about. However, this protection is limited.

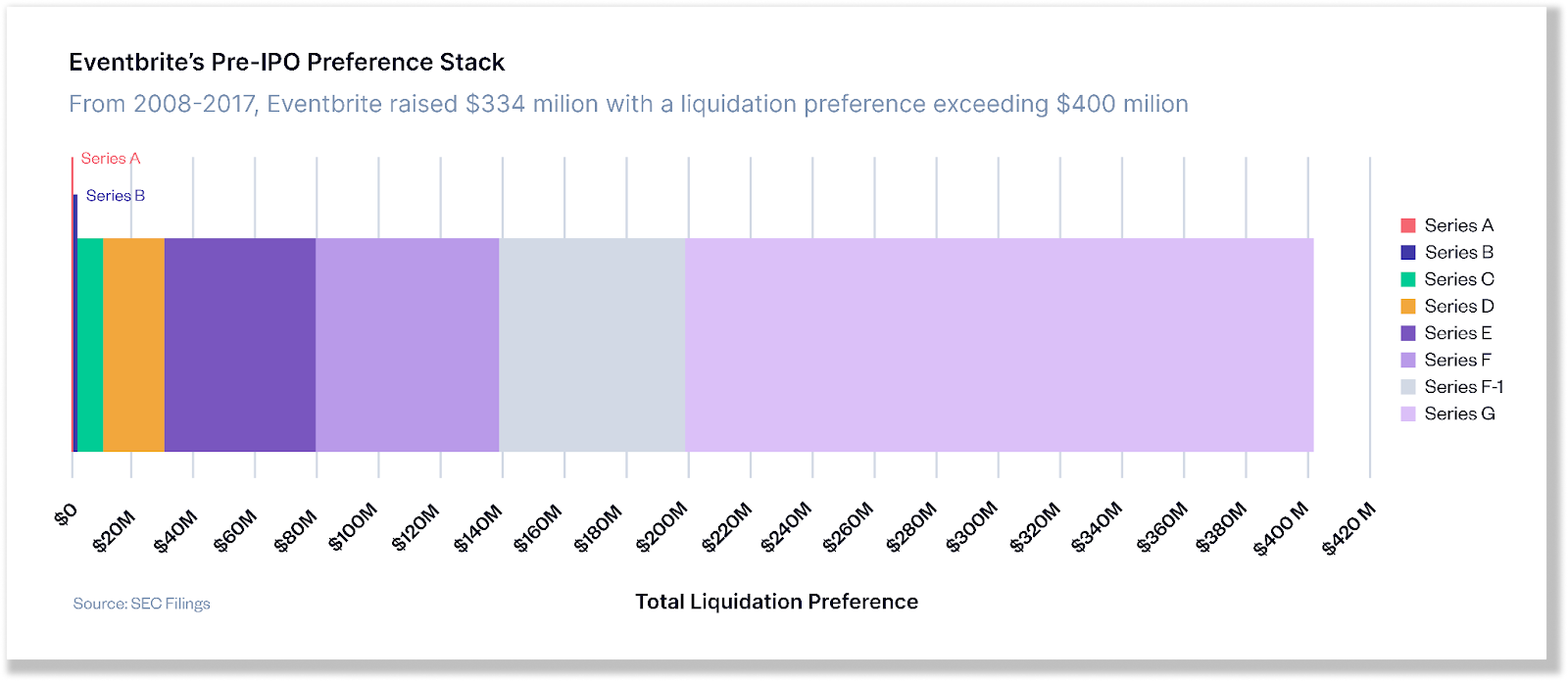

A growing startup often has multiple financing rounds, each with a liquidation preference. You could have a cap table with Ordinary shares, Series-A shares, Series-B shares, and Series-C shares. In that stack, the Series-C investor must get all their money back first, followed by the Series-B and Series-A investors, before proceeds are distributed amongst ordinary shareholders. Multiple liquidation preferences dilute the downside protection of earlier investors.

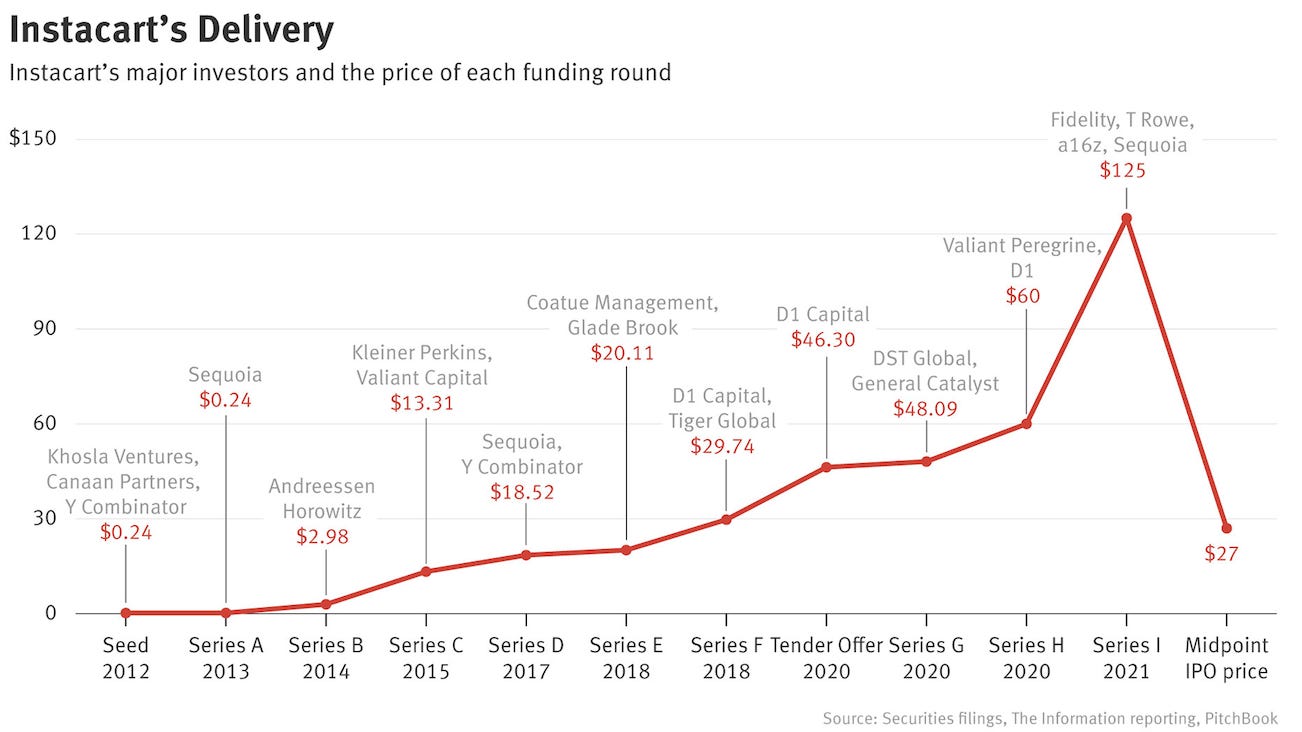

Consider Instacart as an example. Their last fundraise was a $265m Series-I round at a $39bn valuation. If another company acquired Instacart for $265m, only the Series-I investors would get their money back. None of the earlier VCs would get downside protection from their liquidation preferences.

In reality, the Instacart story played out worse. They had an IPO at a valuation below their last VC round. And since IPOs trigger the automatic conversion of preference shares into ordinary shares, there’s no liquidation preference to enforce. All post-Series-F investors in the Instacart IPO lost money!

So liquidation preferences don’t always offer downside protection. In fact outside of IPOs, and more typically in M&A situations, investment returns have to cascade down a multi-level preference stack. Moreover there are situations where VCs with a preference might have to forgo some of it to incentivise other shareholders to play ball when a company is being sold at a low value.

The Upside Motive

As complicated as things might be on the downside, liquidation preferences do something important in the opposite direction. They have an upside thrust that incentivises founders to maximise honesty and outcomes.

Let’s start with honesty. If a VC invests £5m into a company at a £20m valuation, the founders have to be honest in their assessment of the company’s value. If they overstate or, for example, misrepresent it by concealing liabilities, they put themselves at a disadvantage. The company must grow a lot more before the liquidation preference falls away.

The second upside incentive relates to outcomes. Since liquidation preferences are triggered when a company doesn’t grow beyond the last post-money valuation, entrepreneurs are incentivised to build significant value. Only then do liquidation preferences fall away, as we saw in the upside scenario in the earlier table.

Liquidation preferences aren’t much liked by founders. They seem uneven-handed: An outcome that would otherwise be good for ordinary shareholders is hampered by liquidation preferences. Despite the initial optics though, the instrument plays a critical role in aligning incentives and driving outcomes. And it isn’t just about the downside. It’s also about maximising the upside.

Other Updates

I built a custom GPT bot that draws from the knowledge of sixty 20VC podcast episodes. You can read about how I built a rapid prototype here.