What's the optimal number of investments for an early-stage fund?

Three proven strategies to consider: the artisan, goldilocks, or variety index approach.

Hi all! If you’re already a subscriber feel free to dive right into this week’s edition. 👇🏾

If you’re new, a warm welcome and thank you for subscribing! This newsletter shares the best VC wisdom and knowledge curated from seasoned investors, researchers, and technologists.

You’re part of 300+ industry insiders who’ve joined along on a journey to mastery & impact.🚀

Early-stage venture firms engage a kaleidoscope of investing styles. Yet, if a firm decides to launch a fund, there's a simple question that every team must answer: how many investments will you make?

A small portfolio is easier to manage but limits the chances of catching an outlier. In contrast, an extensive portfolio may have a greater probability of successful outliers, but rapid fire investing puts pressure on the quality of deal selection and portfolio value-add, which impact overall returns. (See the notes1 section of this post if you'd like to learn more about the mathematical principles and nuances of portfolio construction.)

What do VCs do in practice? There are a variety of optimal strategies depending on the nature of the firm, its resources, the quality of its team, and its deal selection skills. Consider the spectrum of these three successful early-stage funds in the UK.

The Artisan Approach: Hoxton Ventures

Firms that lean into their selection skill and quality of deal flow typically take the artisan approach, investing in 20 to 25 investments per fund. One example is Hoxton Ventures Fund I. It launched in 2013 with £25m (~ $40m) to invest in roughly 20 companies.

Ultimately, the fund made 18 investments and yielded 3 IPOs (Deliveroo, Darktrace, Babylon) plus 7 acquisitions. The selective focus did not limit Hoxton's ability to source and invest in several incredible outliers. Being picky works for them. It's an effective firm strategy, succinctly declared on their portfolio page: "We pick winners. Winners pick us."

The artisan venture approach works best with small teams that excel at deal flow, selection, and winning the best founders over. Firms that have succeeded with this strategy include Union Square Ventures, Benchmark Capital, and Hummingbird VC.2

The Goldilocks Portfolio Approach: Passion Capital

Is it possible to get the best of both worlds by investing in a high enough number of startups to improve the chances of finding outliers without compromising overall fund quality? Many early-stage firms attempt this by investing in roughly 25 to 50 investment per fund.

Take Passion Capital Fund I as an example. It launched in 2011 with £37.5m ($60m) to deploy in pre-seed and seed-stage businesses. Their target was 50 companies. They eventually invested in 42 businesses and the big wins from that fund include Monzo (worth over $4bn), Gocardless (worth $2bn), and Tray.io (estimated to be worth $600m+). Other modest but notable wins include Mendeley (acquired for $70-100m) and Pusher (acquired for $35m in cash).

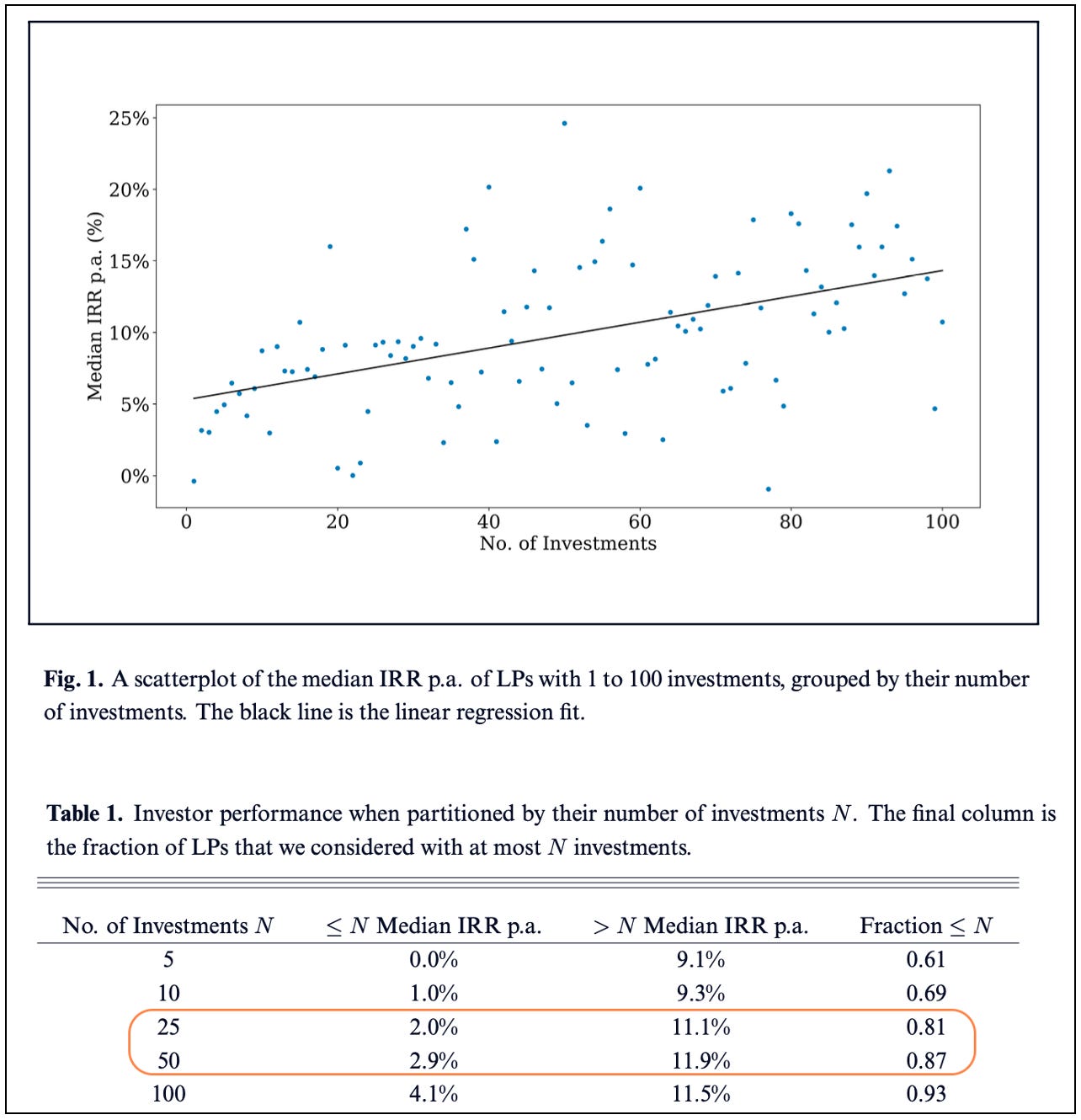

Going for the Goldilocks zone of portfolio construction (25-50 investments) is mathematically sound for returns (see the chart below from AngelList), and it’s a manageable sweet spot for medium-sized VC teams.

Notable firms here include LocalGlobe (e.g. fund VII had £45m and a target of 50 investments) and Creandum (although their first fund was more artisanal with just 10 investments).

The Variety Index Approach: Seedcamp

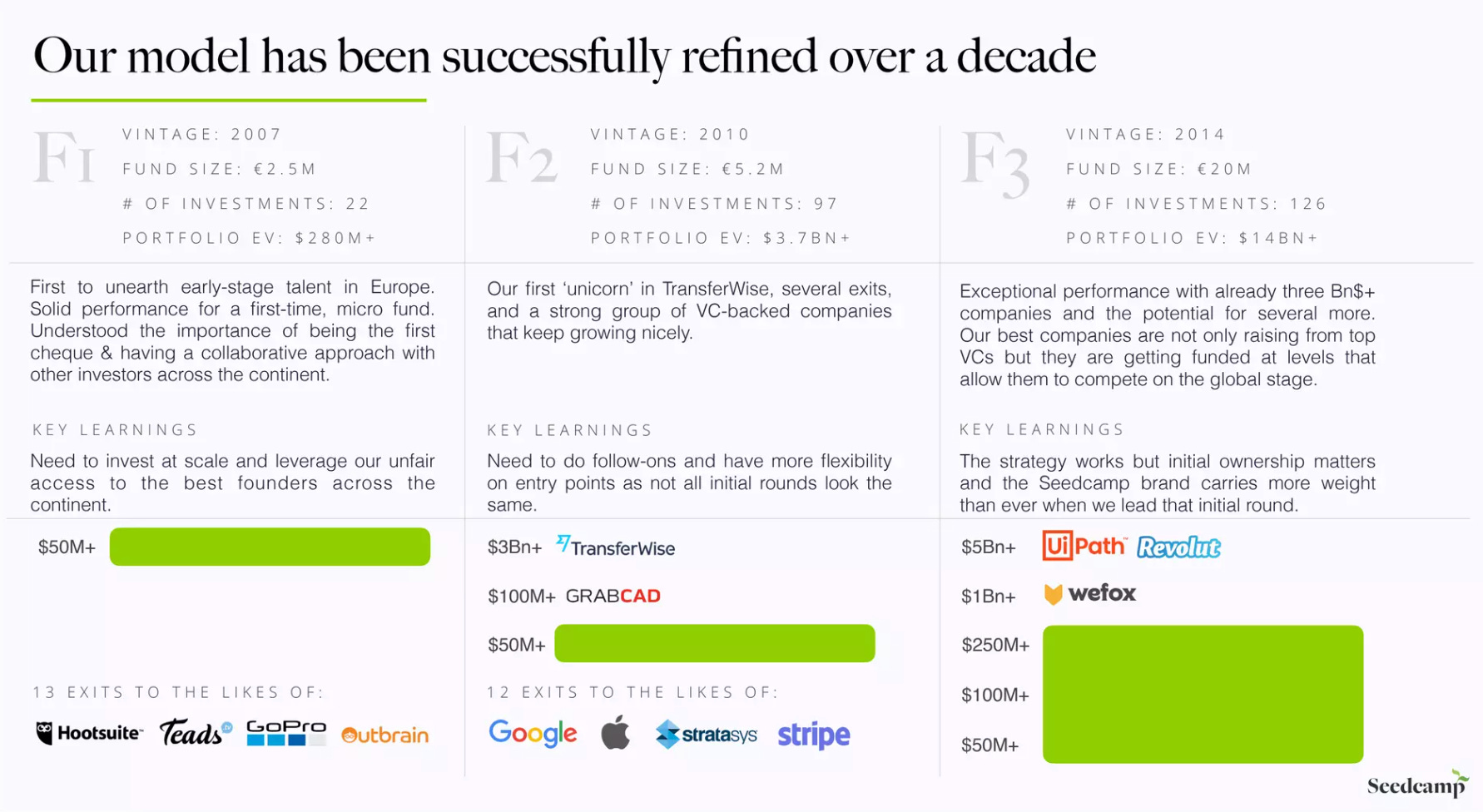

Since power laws drive venture capital success, your investment volume can significantly impact returns. Put another way, the more shots you take, the more likely you are to score big.3 Seedcamp grew to employ this strategy, as shown in the page below from their Fund V fundraising deck.

Their performance has been stellar. IPOs include UiPath and Wise, and over a dozen exits through M&A. Seedcamp intentionally seeks to maximise portfolio diversity across Europe, investing in over 30 companies a year and generating alpha through an indexing approach. They have a small partnership but have invested heavily in the infrastructure and an operational team to support 100+ companies per fund.

Other firms that take this approach include Speedinvest, Precursor Ventures, Kima Ventures, and 500 Startups.

Note that volume isn't everything. For example, market conditions, the quality of your investment decisions, your reputation (and, therefore, whether founders choose to partner with you) all impact outcomes. This is why, for example, portfolio size only accounted for some 20% of the variance in performance in this AngelList dataset.

What's the best approach?

There’s no single ‘best’ approach. Some strategies are definitely inferior though. For instance, if you invest in too few companies, you may not have enough shots at goal to succeed. Alternatively, investing in hundreds of companies without the infrastructure to make it viable or the selection skill to limit losses is wasteful. However, somewhere between these extremes lies a strategy that will work for a particular team with specific skills, resources, networks, and market opportunities.

🥡 Practical takeaway:

Emerging managers4 with small fund sizes and teams should consider the artisan or Goldilocks approach, depending on how bullish they are about their selection skills and access to opportunities with unicorn potential or greater.

On the other hand, established early-stage funds have to pursue a Goldlicks or indexing approach, given how impractical it is to deploy, say, a £250m seed fund artisan-style, backing just 20-25 seed deals.

For an exploration of the mathematical principles and other market nuances that impact the relationship between deal volume and fund performance, see the papers below:

Does Venture Capital Portfolio Size Matter? (2013) This paper finds that when VCs raise more considerable funds, they increase their portfolio size, and this negatively impacts performance. More specifically, a 1% increase in portfolio size reduces IPO or acquisition rates by 2.2%. This is partially the result of diseconomies of scale in venture and the limits to human capital.

How Portfolio Size Affects Early-Stage Venture Returns (2020). This research from AngelList analyses the portfolios of 10,000+ investors on their platform. They find that, on average, each additional investment increases median annual returns by 0.09%.

The Science of Startup Investing (2022). This analysis considers UK startup data and proprietary fund data from their firm. It finds that investors with consistently high returns tend to be the ones with the largest portfolios. The authors propose an index approach to seed-stage investing: 50 deals a year.

Venture Capital Portfolio Construction (2023). This is one of the most nuanced analyses I've come across. I replicated some of this team's findings with Monte Carlo simulations, but if you can't do that, try their simulator here. The key takeaway: Larger portfolios improve the probability of returning 2-5x of a fund, but a very large portfolio dilutes the positive impact of outliers. Other factors, such as decision quality, return potential of each deal, follow-on strategies, fund and the average cheque size, all impact outcomes.

There are many other funds worth noting in this category such as Sequoia’s first fund, as well as Forerunner Ventures’ debut fund in 2010-12.

Power laws also exist in the content business. With my own newsletter I imagine that if I wrote just 5 posts year, the chances of an article going viral would be exceptionally low compared to if I wrote 50. But to do well overall, all articles would need some minimum threshold of quality.

New fund managers who are already known as successful angel investors or ex-operators can afford to take a more artisanal approach with their debut fund, provided they have access to high-quality deal flow and reputations to help them win deals (a great example of this is Sequoia’s founder, Don Valentine.) After all, if they can generate high quality deal flow and pick better companies, there’s less of a need for a large portfolio.