The Venture Capital Funnel: A Marathon of Ambition

The Venture Capital Funnel: A Marathon of Ambition

Why meeting hundreds (and potentially thousands) of founders makes sense.

The venture business is a numbers game. Unless you’re exceptionally lucky, you need enough shots on goal to strike an outlier. But how many shots is “enough”, and what does it take to find the best shots possible?

I explored the first question in a previous post, and now, I’d like to tackle the second: How many investment opportunities do VCs review, and what does the “sales funnel” equivalent of a high-performing investor look like relative to what’s typical.

Higher Performers

Let’s consider one of the first successful venture capitalists—Arthur Rock. His investing career included investments in Scientific Data Systems (acquired by Xerox for $900m), Teledyne (IPO’d), Intel (IPO’d), and Apple (IPO’d). How many opportunities did he review over his working life? According to his estimates, the number is roughly 9,000, though I’m certain the actual figure exceeds 10,000.

“Over the past 30 years, I estimate that I’ve looked at an average of one business plan per day, or about 300 a year, in addition to the large numbers of phone calls and business plans that simply are not appropriate. Of the 300 likely plans, I may invest in only one or two a year…” — Arthur Rock.

More contemporary investors do even greater numbers thanks to a flourishing startup ecosystem. Five years after launching their firm, A16Z were seeing 3,000 deals annually. They would consider 200 startups seriously and invest in 20 each year.

The pandemic in 2020 further transformed the venture landscape. Virtual meetings are now more acceptable, making even greater numbers possible.

Kyle Lui, an investor in several unicorns, doubled the number of founders he met after the pandemic. He went from meeting 20 to 30 founders monthly to anything from 60 to 80.

Some VCs choose to go beyond that. Hummingbird, a firm that’s generated 15-30x returns across its first three funds, reportedly has each team member doing 100 founder calls a month!

These numbers are not typical, and each firm’s approach will vary depending on the investment stage and sector. Still, it’s helpful to know what exceptional cases look like and what high performers do. In contrast, what does a typical funnel look like?

Typical Firms

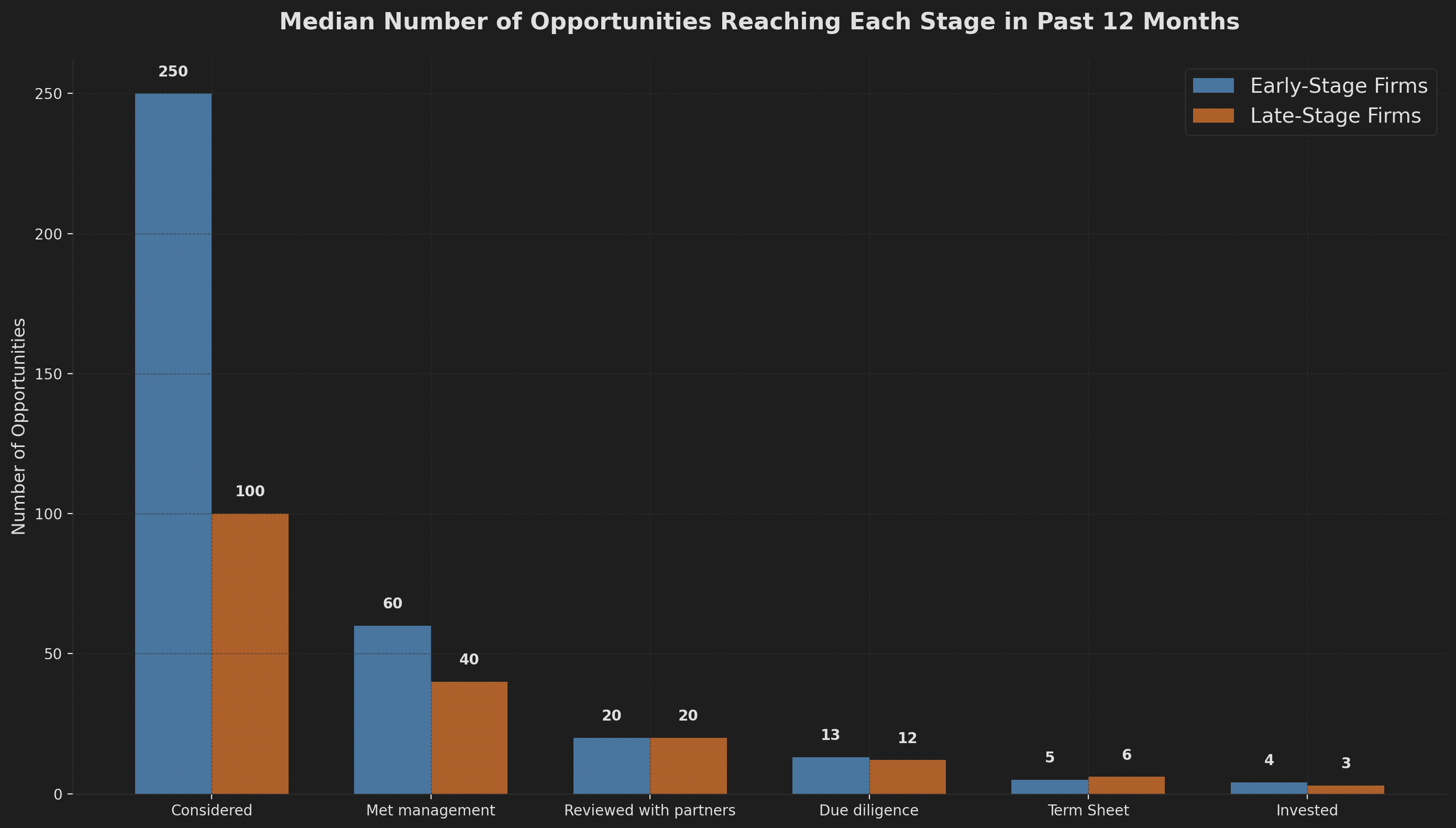

Researchers from Stanford and Harvard surveyed hundreds of VCs to understand what a typical deal funnel looks like. Below is a summary of their findings, split by investment stage.

High Performing VC Funnels

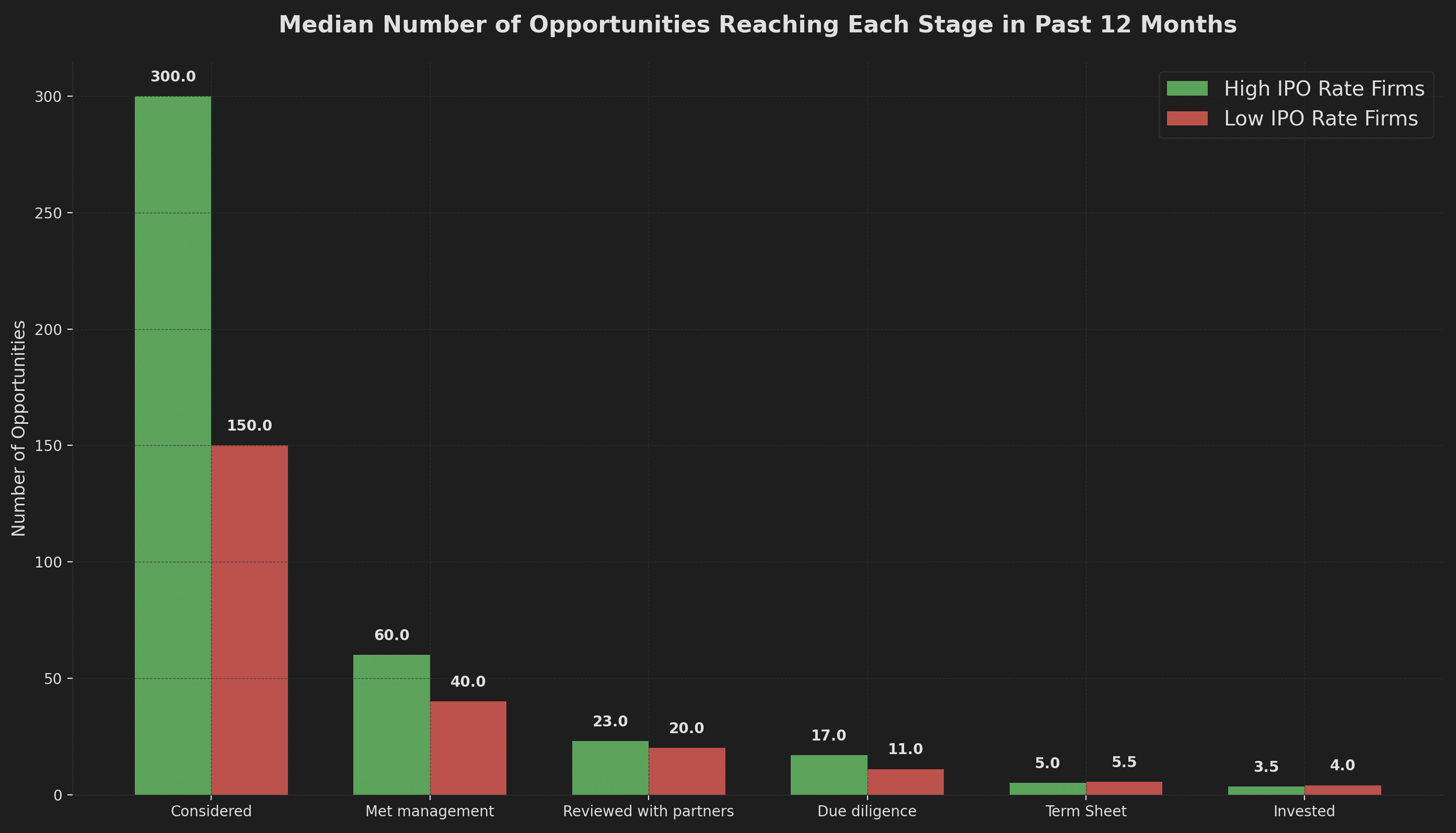

More tellingly, here are the numbers split across two groups: Firms with at least ten exits in the last decade and an above-median IPO percentage rate for those investments (i.e. the High IPO Rate group) versus firms with at least ten exited investments but a below-median IPO percentage rate.

High-performing firms consider 2x more investment opportunities annually at the top of their funnel relative to under-performers. This difference is statistically significant and visible all the way through to the due diligence stage. Although both groups make roughly the same number of investments, one group assesses far more opportunities than the other.

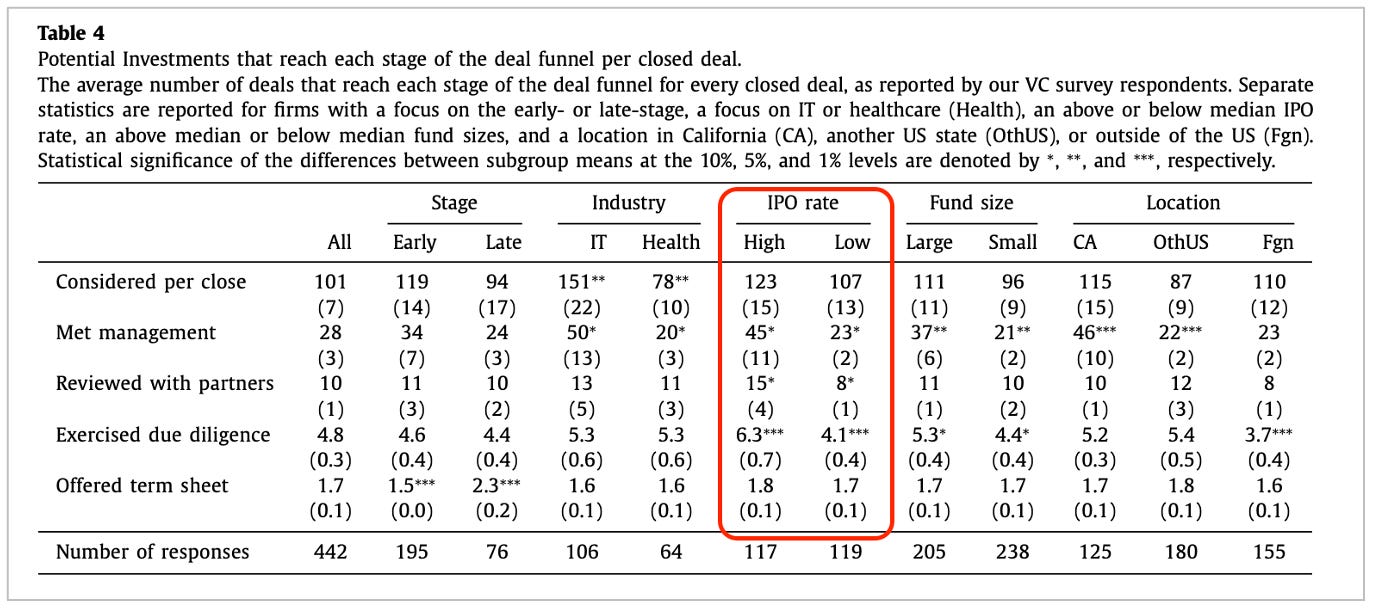

Another cut of the data makes this distinction just as stark. When you consider how many opportunities reach each stage of the funnel per closed deal, high IPO rate VCs review on average 123 opportunities for every 1.8 deals closed. In comparison, VCs with a low IPO rate review 107 opportunities for every 1.7 deals closed. See the table below for more.

Your Numbers Matter

Looking at a VC’s deal funnel is revealing. While meeting lots of founders doesn’t automatically make you a great investor, it achieves at least two critical objectives.

First, you can fine-tune your model of what great looks like using a more meaningful dataset. Football scouts, for instance, review up to eight games a week, assessing 100+ players regularly. Venture is no different. You need to see a lot to know what good looks like.

Second, you’re more likely to find an outlier if you have significant visibility over who’s starting a company and when. More established investors can do this efficiently through their brands, networks, and referrals. However, if you’re just starting out, you have to hustle and thoroughly traverse the founder universe to find great businesses.

None of this is easy. Managing a productive VC funnel requires stamina and smarts.1 But for the select few who can sustain efforts over a decade or longer, finding a unicorn is all in the numbers.

You also have to get good at saying because, in the words of Marc Andreessen, that’s mostly what VCs have to do.